The banking sector in Bangladesh is currently facing an alarming level of capital shortfall. Capital adequacy is one of the most important indicators used to assess a bank’s financial strength. It determines how well a bank can withstand potential risks, particularly financial stress arising from non-performing loans (NPLs).

The Capital to Risk-Weighted Assets Ratio (CRAR) measures the relationship between a bank’s capital and its risk-weighted assets. In line with the international Basel III banking framework, Bangladesh Bank monitors this ratio for the country’s commercial banks. Under regulatory requirements, banks are expected to maintain a minimum CRAR of 12.50% to safeguard depositors’ funds and reduce the risk of insolvency. However, many banks have failed to maintain the required provisions or loan-loss reserves against the large volume of defaulted loans.

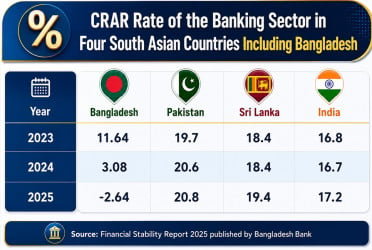

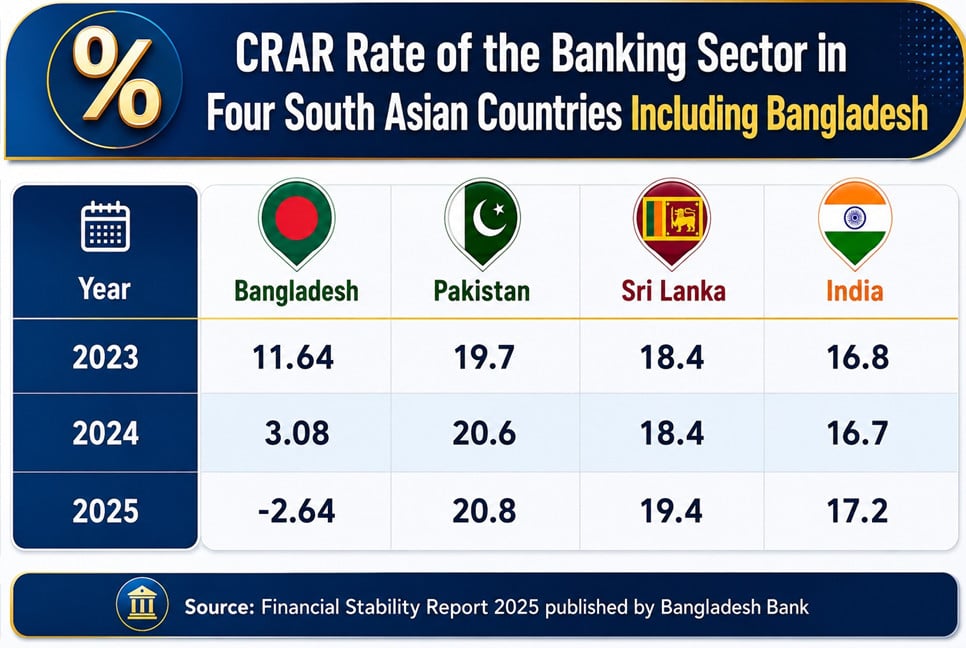

According to central bank data, the average CRAR of Bangladesh’s banking sector fell to negative 2.64% at the end of last year, far below the Basel III minimum requirement of 12.50%. Sector experts note that it is extremely rare in the modern world for the average capital adequacy ratio of a functioning country’s banking sector to turn negative. They view the development as a deeply concerning signal for Bangladesh’s financial system.

While the banking sectors of neighbouring India, Pakistan and Sri Lanka have strengthened, Bangladesh’s banking sector has moved into negative capital territory. Pakistan’s banking sector now has a CRAR of nearly 21%, while Sri Lanka’s exceeds 19%. According to Bangladesh Bank’s Financial Stability Report 2025, India’s banks have an average CRAR of 17.20%. This comes despite the fact that both Pakistan and Sri Lanka faced severe economic crises only three years ago, marked by foreign exchange shortages, soaring inflation and economic stagnation.

A negative capital adequacy ratio is generally regarded as an indicator of banking sector insolvency. Bangladesh Bank data show that nearly two dozen banks in the country are currently suffering from capital deficits. Their combined capital shortfall exceeds Tk280,000 crore. Industry insiders say the deficit would have been several times larger had the central bank not granted regulatory forbearance regarding provisioning requirements.

Bangladesh Bank itself considers the situation highly unusual. Arif Hossain Khan, Executive Director and spokesperson of the central bank, said: “It is difficult to find another country in the modern world whose banking sector has a negative CRAR. In that sense, Bangladesh’s case is indeed rare. Capital shortages begin with provisioning shortfalls, which become severe when defaulted loans rise abnormally. The scale of non-performing loans we are seeing today is not the result of normal banking activities; rather, it reflects the looting of banks through the lending system.”

He added: “The fraudulent lending practices that took place in some banks after 2009 cannot be described as banking in any meaningful sense. It would be more accurate to call it plunder. Those who took these loans are not borrowers but looters. We are now being forced to inject liquidity through money creation to support depositors in looted banks. This cannot continue indefinitely. If it does, Bangladesh could face inflationary pressures comparable to those experienced by Zimbabwe or Argentina.”

Bangladesh Bank publishes its annual Financial Stability Report to assess the overall condition, risks and stability of the country’s financial sector. The latest edition shows that the banking sector’s CRAR stood at 11.64% at the end of 2023. By the end of 2024, it had fallen sharply to 3.08%, before plunging further to negative 2.64% at the end of 2025.

At the same time, neighbouring countries have strengthened their banking sectors. According to the report, India’s banking sector CRAR increased from 16.8% in 2023 to 17.20% last year. Pakistan now has the strongest capital structure among South Asian banking systems. Despite recent economic turmoil, its CRAR stood at 19.7% in 2023 and rose further to 20.80% in 2025.

Sri Lanka’s banking sector also remains well-capitalised. Its CRAR reached 19.40% last year, up from 18.4% in 2023. This is particularly notable given that Sri Lanka’s economy faced a sovereign debt crisis following the Covid-19 pandemic, which led to the collapse of the Rajapaksa government and inflation peaking at 69% in September 2022.

Bank executives and policymakers argue that non-performing loans were concealed during the Awami League’s 15-year rule. Banks controlled by oligarchic and mafia-like business groups were often not subjected to proper audits, while central bank oversight was inadequate in many cases. Following the mass uprising led by students and citizens in August 2024, hidden bad loans began to emerge. As a result, the rapid increase in NPLs has pushed the sector’s CRAR into negative territory within a short period.

Despite the broader crisis, several banks continue to maintain strong capital positions, according to Association of Bankers, Bangladesh (ABB) Chairman Masrur Arefin. The Managing Director of City Bank PLC said: “There are large private-sector banks in Bangladesh with CRARs ranging between 17 and 20%, including City Bank. Banks that follow sound corporate governance have focused on strengthening their capital structures. The problem is that the CRARs of banks affected by irregularities and corruption have deteriorated so severely that they have dragged down the entire sector. This is damaging the international reputation of Bangladesh’s banking industry and affecting the country’s overall ratings.”

The main driver behind the negative CRAR is the rapid growth of non-performing loans. In June 2024, total NPLs stood at Tk211,391 crore, representing 12.56% of outstanding loans. The figure continued to rise, reaching Tk644,515 crore by September 2025, equivalent to 35.73% of all loans. Although regulatory concessions and loan rescheduling reduced the figure somewhat during the final quarter of last year, NPLs still amounted to Tk588,704 crore at the end of March this year, representing 32.26% of total loans.

While nearly one-third of all loans in Bangladesh are now non-performing, the ratio is only 2.2% in India and 5.8% in Pakistan. Even in Sri Lanka, which experienced a recent economic collapse, the NPL ratio remains in single digits.

The severity of the capital crisis is reflected in the financial statements of state-owned Janata Bank. At the end of last year, the bank’s actual capital shortfall had reached Tk64,406 crore—almost double the cost of constructing the Padma Bridge. Without regulatory relief on provisioning requirements, Islami Bank Bangladesh PLC’s capital deficit would exceed Tk70,000 crore. Similarly, the combined capital deficit of the five Shariah-based banks set to be merged into a consolidated Islami Bank would exceed Tk150,000 crore.

Former Finance Secretary and former Sonali Bank Chairman Mohammad Muslim Chowdhury described the negative CRAR and capital deficit as “frightening”.

“The situation is extremely serious,” he said. “In the modern era of banking, it is abnormal and almost unimaginable for a country’s banking sector to have a negative CRAR. The situation speaks for itself. I urge the government and Bangladesh Bank to address the issue with the utmost seriousness.”

Basel III standards were introduced internationally to ensure banks have sufficient capital to absorb losses during financial crises and periods of severe stress. The framework aims to ensure that banks can continue operating using their own capital even during times of crisis. While Basel III has long been implemented in advanced economies, Bangladesh began adopting the framework in 2015, with full implementation initially targeted by 2019. Under the framework, banks are required to maintain capital equivalent to 12.5% of their risk-weighted assets. Yet Bangladesh’s banking sector has now fallen into negative capital adequacy territory.

Source: Bonik Barta